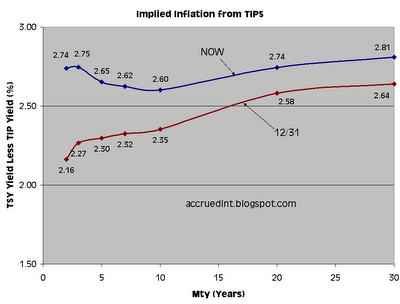

Is inflation going to accelerate from here? The market for inflation-protected Treasuries (TIPS) is telling us no. TIPS pay a normal coupon, but the principal amount of the security also increases based on CPI. So making a slight simplification, the annualized total return on a TIP held to maturity will be Yield + CPI, whereas the same return on a traditional Treasury bond is just its Yield. Subtract the stated yield of a TIP from a similar maturity Treasury, and you get market’s expectation of CPI.

We can string together different implied inflation figures for different time periods to create an inflation curve. Just like the yield curve should be a predictor of future interest rates, the inflation curve should be a predictor of future inflation. For example, the yield differential between a 3-year Treasury and a 3-year TIP should be approximately equal to the average CPI level over the next 3-years. The graph below shows the current inflation curve compared with the curve on 12/31/05.

Back in December, the curve was positively sloped, implying that market participants saw long-term inflation as being higher, on average, than near-term inflation. Today we see the entire curve is much higher than it was at the beginning of the year, but we also see that it is inverted between 2 and 10 years. Note that CPI prints have been between 3.5 and 4% for most of the last 12-months, so the implied 2.74% for the next two years is a significant deceleration in itself. But the curve being inverted tells us that market participants expect even more deceleration of inflation in the long-run. Doing some quick math and ignoring minor details like the time value of money, if the average CPI is going to be 2.75% over the next 3 years, but only 2.60% over the next 10-years, then the average from years 3 through 10 has to be about 2.5%. The Fed would probably be happy with a figure like 2.5% for overall CPI. I think the implied inflation curve is going to be a great indicator of when the Fed will do. If this curve continues to invert, the Fed will become more comfortable with inflation expectations, and a pause is more likely.

Friday, July 07, 2006

![]()

![]()

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment