(Alternative title: 10,000?!?!)

The sub-prime woes of 2007 have thrust bond insurers into the spotlight, and for the first time really calling into question the utility of municipal bond insurance. I have received a number of e-mails and comments from municipal bond investors expressing concern over the quality of their portfolio. I thought it would therefore be useful to discuss how muni insurance works, and what the decline of any municipal insurer would mean for municipal credit quality.

Municipal?

First a couple notes about municipal bonds. The term "municipal" is a bit of a misnomer, since any tax-exempt bond is generally considered a "municipal." That includes not only states, counties, and cities, but also government-related entities (such as a public university) and non-profit organizations (such as a hospital or private university). States, cities, counties and school district bonds which have pledged their full taxing power to bond holders are called general obligation. All other issues are called revenue bonds. Readers should note that governmental authorities are often not funded out of the state's general revenue, but out of their own revenue stream. For example, the Maryland Transportation Authority's revenues come from tolls and the state fuel tax. It would be theoretically possible for the Transportation Authority to be bankrupt without the state defaulting on anything.

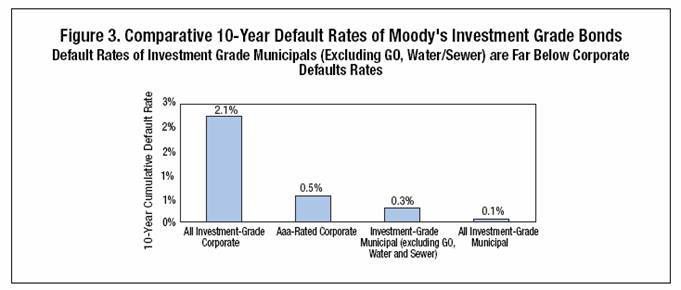

"Zero Loss"

Municipal default rates are far lower than their corporate counterparts, as the following chart from Moody's shows.

In fact, there has been only one General Obligation issuer rated by Moody's which defaulted since 1970, and in that case, the default was cured (paid in full) 15 days later.

Certain revenue issues are considered so fundamental to the operation of the government that the odds are low that any government would allow the issuer to fail. These bonds are called essential service bonds and bonds within this category also have a very low default rate. There is no one definition of essential services, but typically issues for public universities, primary/secondary schools, water and sewer utilities, and state highway authorities fall within this category.

The Aaa-rated insurers, MBIA, AMBAC, FSA, FGIC, XLCA, Assured Guaranty, and CIFG, have historically insured mostly general obligation and essential service bonds. MBIA has a self-described "zero loss" underwriting standard, so concentrating their insurance activities within a very low default risk arena seems to fit.

The Aaa insurers have and do insure other issues, like hospitals or industrial development bonds. But the insurers charge much more for these kinds of projects, and often demand some hefty protection in terms of covenants or pledges. In past talks with people working for insurers, my understanding is that they believe every bond they insure has risk equivalent to a Aa-rated corporate bond or better.

"We could almost buy our own ship for that!"

Now you may be wondering if insurers are underwriting to a zero loss, why do municipal buyers bother with insurance? Well, municipal buyers tend to be very high quality focused. In essence, the municipal investor wants to take advantage of the tax-exemption, s/he isn't real interested in credit risk. So having bond insurance allows the muni buyer to do minimal credit research (if any) before buying a bond. This facilitates liquidity in the muni market, because Street traders can put a reasonable bid on any insured bond without having particular knowledge of the underlying credit.

Who buys the insurance?

Municipals are initially sold to the public through underwriters just like stocks or corporate bonds. The underwriter may be selected in advance (called a negotiated deal) or by competitive bid (called a competitive deal. No really!). In a negotiated deal, the underwriter and issuer jointly decide whether to insure the bond or not. They will solicit bids from various insurers and determine whether the cost of insuring the bond lowers the rate on the bond enough to make insurance worth it. In a competitive deal, the underwriter presents a bid to the issuer, which is an all-in cost of the bonds, including issuance costs and interest rate. If the bonds are to be insured, that's just part of the issuance cost.

In a competitive deal, its often the case that the insurer is contacted about insurance only a couple hours before the bids are due. In the case of essential service bonds with an explicit rating or that the insurer has insured before, the turnaround time on an insurance bid can be mere minutes.

Technically the insurance is bought by investors, as the cost of insurance is taken out the proceeds of the bond sale. It is almost always paid as a lump sum to the insurer when the bond sale settles.

How much does the insurance cost?

Insurance may cost less than 10 basis points as a percentage of the bond deal its an essential service deal with a strong underlying rating. Riskier deals obviously cost more. This highlights why most investors wanted the insurance: it is usually so cheap, why not buy the insurance?

Here it might be helpful to think of municipal insurance the same way you think of homeowners insurance. Everyone knows that if you simply look at the odds of making a claim vs. the cost of insurance, buying insurance is a net negative for the home owner. However, most homeowners would be bankrupt in the event that their home was destroyed, as they would not be able to repay their mortgage. The negative ramifications of this relatively low probability event are so high that home owners willingly buy insurance, knowing its a net negative proposition. Municipal insurance is the same way.

What percentage of municipal bonds are insured?

About 45% of investment-grade munis are insured. In practice, there are two major types of bonds that don't get insured. First is lower-rated issuers, which the insurers either won't insure or for which the price is too high. This would be your A or Baa-rated hospitals, nursing homes, development projects, etc. Sometimes these kinds of issues are insured, and sometimes they are not. If they are not, buyer beware. An insurer probably wanted to charge an arm and a leg because they viewed the bond as risky.

Second is higher-rated issuers. Obviously "natural" Aaa-rated issuers don't need insurance. But also many Aa-rated issuers, especially large and well-known issuers, don't benefit much from insurance. For example, the State of Florida is Aa-rated, but rarely buys insurance for their issues because their credit is well-known. Conversely a school district in rural Kansas would probably pay for the insurance, even if they would have a Aa-rating on their own, because buyers are not familiar with the credit.

Do insured bonds trade with the same yield as other Aaa-rated bonds?

No. Natural Aaa-rated issues typically yield about 10bps less than insured issues. Historically, insured issues trade very similarly to strong Aa-rated issues. Hence why larger, well-known Aa issuers usually don't get insurance.

So what happens if an insured bond defaults?

The insurance policies state that the insurer will pay timely principal and interest. Translated, this means that the insurer will make all payments as though nothing happened to the underlying issuer.

So what happens if an insurer defaults?

Nothing changes about the municipal issuer's obligations to pay investors. Remember that the cost of insurance was paid up front. There are no on-going payments, so neither the investor nor the issuer would have any claim against the insurer so long as the issuer remained solvent.

What about the ratings? What is an underlying rating?

Even when a bond is going to be issued with insurance, it is common for issuers to get a rating "on their own." This rating is called an underlying rating.

So if the insurer were to be downgraded, the bond's rating would revert to the greater of the insurer's rating or the underlying rating.

Why not get an underlying rating?

S&P and Moody's charge issuers an exorbitant fee for a rating, so often smaller issuers or issues done for a one-off project don't get underlying ratings. Sometimes issuers choose to buy the insurance because insurance was cheaper than getting a rating.

A good example of a one-off project would be a deal I bought a while back for a new electrical substation at Georgia Tech University. GA Tech structured the deal such that it was off-balance sheet: they issued the bonds under their Foundation and then the Foundation leased the substation back to the university. A deal like that is unlikely to get an underlying rating for two reasons. First, its a one-time project, so paying for the rating would not have on-going benefits. Second, GA Tech is well known and the substation is obviously extremely important to the University. Investors logically assumed the rating would be about the same at the University's rating.

Up until recently, another category of issuers who did not get underlyings would be those that expected a Baa underlying. It was often assumed that having a Baa underlying would not improve the rate investors would pay, especially in the case of a general obligation issue. Now that is changing, as investors don't want to wind up with a non-rated bond in the event that the insurer is out of the picture.

What about trading levels in FGIC and XLCA bonds?

I think until either is downgraded, you won't see much trade. And it will depend greatly on the underlying rating.

What's the future for insurance?

I believe that insurance will continue to be a major part of the municipal market. I expect two major changes:

- Somewhat fewer bonds will come insured, especially if they were Aa-rated on their own.

- Very few issues will come with no underlying, even if its a Baa underlying. Many investors are restricted from owning non-rated bonds, so therefore even a weak underlying would allow the investor to continue to hold the bond.

But the basic advantage of owning insurance hasn't fundamentally changed.

10 comments:

""So what happens if an insured bond defaults?

The insurance policies state that the insurer will pay timely principal and interest. Translated, this means that the insurer will make all payments as though nothing happened to the underlying issuer.""

If this happens, would there be any change in the chances that the bond might get called on or after the call date? Also, would the insurer be just as likely to do a refunding as would the issuer?

That's a good question. If the issuer were in liquidation, then I'd suspect the question to call or not to call depends on the cost of capital to the insurer.

The cases of defaults which I'm more familiar with resulted in the issuer eventually emerging from BK and making the insurer whole. In those cases obviously the issue was called or not based on normal interest rate considerations.

""Certain revenue issues are considered so fundamental to the operation of the government that the odds are low that any government would allow the issuer to fail. These bonds are called essential service bonds and bonds within this category also have a very low default rate. There is no one definition of essential services, but typically issues for public universities, primary/secondary schools, water and sewer utilities, and state highway authorities fall within this category.""

Let's never forget the famous default of the Washington Power case in the early 1980's when holders of the non-insured tranche got killed while the insured tranche got paid in full.

""On December 24, 1988, the parties in the various lawsuits reached a settlement of $753 million. Some of the 30,000 bond holders would receive 40 cents on every dollar invested and others got as little as 10 cents. Because a court found that some of the bond monies for Plants 4 and 5 were spent on Plants 1 and 3, participants in those projects were held liable for the default. Seattle's share was $50 million, of which $43.2 million came from insurance companies. The last settlement was reached in 1995.

http://www.historylink.org/essays/output.cfm?file_id=5482

and....timeline 1983...

""1983 Financial Guaranty Insurance Company (FGIC) is formed. The percentage of newly issued municipal bonds that are insured reaches 10%.

Washington Public Power Supply System defaults on debt payments. Investors holding uninsured WPPSS bonds experience delays and reductions in payments, while holders of the insured bonds receive interest payments in full, on schedule. The WPPSS default was a turning point in the municipal market, vividly illustrating the value of bond insurance.""

http://www.afgi.org/facts-tline.htm

Regarding calls on insured bonds that default - The insurance company has the requirement to pay interest and principal promptly but they also have the right to call the bond at par in the event of default. So be careful if the underlying credit is weak but the bond is trading at a big premium because of the insurance.

hi,

not a bond related question but a nagging one nonetheless:which Episode of SW did that '10,000' quote come from?

Anon: I remember in the late 90's hospitals doing insured deals at deep original issue discounts for that exact reason. Investors were willing to take less spread if they knew they'd be protected from losing money in a default-then-call situation

Fred: Cantina scene. Han quotes 10,000 to take Luke and Obi Wan to Alderaan. Luke says "10,000?!? We could almost buy our own ship for that!"

Thanks! You got me stumped there. Think it's time to re-watch SW Ep V...

Cheers

Fred

I mean episode IV!

Great blog post. Are you aware of where I could find any information or data that addresses the number of insured municipal bond issuers v. uninsured municipal bond issuers in 2006 v. 2007? I would also be interested in specifically examining the spreads of of AAA-insured v. AA-uninsured for those same years.

really thankful to you for the information sharing...

really nice blog...

Post a Comment